A constant in the history of money is that every remedy is reliably a source of new abuse.

John Kenneth Galbraith, Money: whence it came, where it went

For as long as money has existed in its two most popular forms – either as debt-based accounting systems or as notes and coins – it has had its critics. Some think there is too little of the stuff and others think there is too much, depending on your point of view, or more crucially, your existing wealth.

This is how a leading historian of money describes the historical pendulum swing between these two poles:

We shall see as our history of money unfolds that there is an unceasing conflict between the interests of debtors, who seek to enlarge the quantity of money and who seek busily to find acceptable substitutes, and the interests of creditors, who seek to maintain or increase the value of money by limiting its supply, by refusing substitutes or accepting them with great reluctance, and generally trying in all sorts of ways to safeguard the quality of money.i

So the history of money is also the history of proposals for money reform.

Increasing the quantity of money

Before the modern era, kings and emperors always held a monopoly on the official money supply. Licensing the mints to create the ‘coin of the realm’ was a lucrative business for rulers. Generally, they tended to allow enough money to be created to meet their own needs but there was often greater demand for money at the local level than the ‘legal tender’ money could supply. Into this gap stepped the counterfeiters, who created money to look like the official stuff. If they were caught, they would be executed because rulers viewed such activity as equivalent to murder but that did not stop many trying because that too was a profitable business.

From about 700 AD to 1800 AD, England’s coinage was mainly a marriage of silver and gold. The Spanish conquest of new gold and silver mines in South America was also exploited by English and Dutch pirates, who were officially licensed by their governments as ‘privateers’ to intercept and plunder the Spanish ships. The result was a large influx of new money into Europe. In Spain, it led to hoarding by the rich and price inflation in the economy. In northern Europe it tended to encourage commerce. As long as the economy was growing, potential inflation from the new money was kept in check.ii

War and the need for credit

There is a strange symbiotic relationship between war and peace. The need to defeat an enemy makes people very inventive: jet engines, computers, navigation systems – all these technologies were either invented or rapidly developed during the crisis of war and then found new uses in peace time. War also consumes money. That makes those who wage it get creative in developing new monetary instruments that can also be used for peaceful purposes when war ends.

In the late seventeenth century, England was fighting the increasing power of France under King Louis XIV, the ‘Sun King’. England suffered a humiliating naval defeat at the hands of the French in 1690 and needed to rebuild its navy. It desperately needed money. The traditional way to raise money was to go to the money lenders and pay high rates of interest. However, a previous King Charles II had notoriously defaulted on his debts so the moneylenders were reluctant to lend King William the money.

Scotsman William Paterson proposed a bold plan: the creation of a new Bank of England with subscriptions from the public. £1.2 million (roughly £155 million today) was raised within 12 days, half of which was used to rebuild the navy. This great shipbuilding effort created employment, stimulated the economy and paved the way for the rise of the British navy and later a global empire.

The birth of the Bank of England in 1694 also signalled the birth of the ‘national debt’, which has grown along with the economy ever since. Over the last three hundred years, there has been a constant debate about the wisdom of a national debt. There are three typical positions on this question: “pessimist”, “optimist” or “realist”:

Public debt pessimists argue that government provides no truly productive services, that its taxing and borrowing detract from the private economy, while unfairly burdening future generations, and that high and rising public leverage ratios are unsustainable and will likely cause national insolvency and long-term economic ruin…

Public debt optimists believe that government provides not only productive services, such as infrastructure and social insurance, but means to mitigate what they perceive to be “market failures,” including savings gluts, economic depressions, inflation, and secular stagnation. Optimists contend that deficit-spending and public debt accumulation can stimulate or sustain economy activity and ensure full employment, without burdening present or future generations…

Public debt realists contend that government can and should provide certain productive services, mainly national defense, police protection, courts of justice, and basic infrastructure, but that social and redistributive schemes tend to undermine national prosperity. Realists say public debt should fund only services and projects that help a free economy maximize its potential, and that analysis must be contextualized – i.e., related to a nation’s credit capacity, productivity, and taxable capacity. According to realists, public leverage is neither inevitably harmful, as pessimists say, nor infinite, as optimists say.iii

Great Recoinage of 1696

At first, the new Bank of England only affected those who had invested in it – who earned a handsome 8% return on their investment – and those who benefitted from the new employment opportunities created by rebuilding the navy. Of more concern to most people was the silver coin of the realm used to do daily business. For centuries, both monarchs and counterfeiters had tried to get ‘more bangs for their bucks’ by adulterating the precious metal of official coins with base metals. By the year 1696, English silver coinage was in a sorry state. Years of ‘clipping’ the edges had reduced the value of many coins and, according to one estimate, up to 10% of the coins in circulation were counterfeit. Added to these problems was the ancient conflict between commodity money acting both as a medium of exchange for trade and as a valuable commodity in itself. Silver as a commodity had a higher market value in Paris and Amsterdam than in London, so vast quantities of silver coins were being shipped out of the country and thus no longer in circulation as a medium of exchange.

Isaac Newton, who had already transformed the world with his scientific theories, was invited to apply his knowledge of chemistry and mathematics to rescue the coinage from the counterfeiters and adulterators. Newton approached the problem in a thorough manner. He proposed withdrawing all silver coinage from circulation and issuing new coins. New mints were established at Bristol, Chester, Exeter, Norwich, and York. Old coin could be given back by weight rather than face value. The new strategy did not work. Silver was still worth more when melted down into bullion and sold. Out of this experience, England eventually developed the ‘gold standard’ because gold was perceived to be more stable than silver.iv

Newton also went after the counterfeiters ruthlessly. He cross-examined more than 100 witnesses and personally gathered much of the evidence he needed to prosecute 28 ‘coiners’. One of these was a notorious con man called William Chaloner, who was eventually convicted of high treason and suffered the ultimate gruesome penalty: he was hanged, drawn and quartered.v

More war, more debt

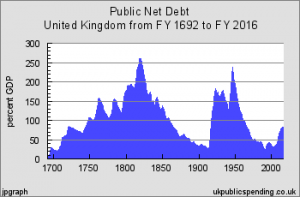

The Napoleonic Wars of 1803-181 5 left the British economy in chaos. The national debt was now over one hundred years old and decades of war had only increased it. While an economy is growing, public debt is not necessarily a problem, as there is enough national income to pay back the debt without incurring further debt. The crucial statistic is its relationship to national income (now called Gross Domestic Product or GDP). In 1815, the national debt stood at 200% of GDP, a record ratio it would never again reach. The rapid growth of the industrial revolution and the global trading monopolies of the British empire would later ensure a continual decline of the debt to GDP ratio to a low of about 30% on the eve of the First World War in 1914, after which it shot up again.

5 left the British economy in chaos. The national debt was now over one hundred years old and decades of war had only increased it. While an economy is growing, public debt is not necessarily a problem, as there is enough national income to pay back the debt without incurring further debt. The crucial statistic is its relationship to national income (now called Gross Domestic Product or GDP). In 1815, the national debt stood at 200% of GDP, a record ratio it would never again reach. The rapid growth of the industrial revolution and the global trading monopolies of the British empire would later ensure a continual decline of the debt to GDP ratio to a low of about 30% on the eve of the First World War in 1914, after which it shot up again.

Banking reforms in the nineteenth century

The wars against France from 1789 to 1815, combined with economic conflicts, created a shortage of silver and copper coins. Paper money was legalized in 1797 to help fill the gap. All over the country, local banks and private companies created local notes and tokens.

According to historian Glyn Davies, “By the turn of the century the total supply and velocity of circulation of tokens, foreign coins and other substitutes very probably exceeded those of the official coin of the realm.“vi

This power of local money creation certainly played a dynamic role in empowering entrepreneurs in the early stages of the industrial revolution but it also inevitably led to abuses. Local companies created ‘truck shops’ at which their workers were forced to buy overpriced goods with the tokens their employers had created. Local banks created worthless paper notes and then crashed, leaving their creditors with nothing.

All of these abuses led to calls for reform. A series of banking acts in 1826, 1833 and 1844 made local notes and tokens illegal and began the monopoly of ‘legal tender’ national money in England, Wales and Northern Ireland, which lasts to this day.

The Great Crash, Keynesianism and Monetarism

The greatest monetary event of the early 20th century was the Great Crash on Wall St. in 1929, which sparked a worldwide economic depression. This event clearly showed how interconnected the world economy had become in the preceding century of unprecedented growth fostered by industrial capitalism. It also called into question the orthodoxies of ‘laissez faire’ market based economics and sparked great debates about economic and monetary policy.

The Gold Standard Act of 1925 had obliged the Bank of England to sell gold at a fixed price. But in the economic chaos following the 1929 crash the Bank feared it could not meet its obligations and in 1931 Britain left the gold standard, which gave the government more flexibility in economic policy.

One perceptive observer of these events was the economist John Maynard Keynes who published The General Theory of Employment, Interest and Money in 1936. He called into question the economic theories that seemed to have led to the events of 1929 and after. This book would deeply influence the next generation of economists and policy makers, whose policies came to be known as ‘Keynesian’. These policies generally encourage an increase in the money supply in order to stimulate economic growth.

During the 1960s and 1970s, however, there was a widely observed phenomenon of ‘stagflation’ – a wicked combination of stagnant economic growth, high unemployment and price inflation – that Keynesian theory had no direct answers for. Some non-Keynesian economists argued that UK policy makers had failed to recognize the primary role of monetary policy in controlling inflation. Keynesianism fell out of fashion and the ‘monetarist’ theories of Milton Friedman, which argued for ‘tight money’ policies, were enthusiastically adopted, particularly in the UK and the USA in the early 1980s. Strict monetarism was later relaxed as it did not deliver the economic results it promised and the price in unemployment was so high.

These extreme swings of fashion from one theory to another seemed to confirm Glyn Davies’ ‘pendulum theory’ of monetary history:

There are few things more impressive than the haughty analytical certainty with which fundamental theories of money are for a time almost universally held, only to be discarded in favour of a diametrically opposite but equally firmly and widely held new orthodoxy which in turn lasts until the whole process reverses itself suddenly a generation or so later.vii

Modern calls for reform

Although a few idealists argue for a world without money – and most written utopias abolish money altogether – most people accept that complex, interconnected modern economies need money in some shape or form to function. Only 3% of modern money exists as notes and coins. The rest – from bank loans to mortgages to your monthly salary – is stored as digital records in computers.

Just like the 1929 crash before it, the 2008 economic crash – the biggest in history – unleashed unprecedented questioning of economic and monetary orthodoxies of the preceding generations and reinvigorated debates around various longstanding ideas for monetary reform:

- Reform what gives money its value

- Reform how much money may be created

- require commercial banks, which currently create 97% of the money supply through bank loans and mortgages, to keep 100% reserves

- put a deliberate cap on how much money may be created eg Bitcoin

- Reform who creates money

- remove the power of commercial banks to create money through interest-bearing loans and require a government-controlled and fully owned central bank to create interest-free but repayable loans for public infrastructure and productive private investment

- remove the power of commercial banks to create money through interest-bearing loans and require the Treasury or central bank to create debt-free, non-repayable money rather than the central bank creating new money in the form of interest-bearing bonds

- allow local citizens or business associations or local governments to create complementary currencies.

Monetary Reform Movements

Organised monetary reform movements are relatively small and they face a massive challenge. In our basic education, most of us do not learn about where money comes from, who creates and controls it and for what purposes. Monetary reformers therefore have to first educate and inform before they can mobilise and reform. They have to create a basis of understanding of the existing financial system and its shortcomings in the public mind before they can convince people to consider and campaign for other ways of doing things.

Britain first became a fully representative democracy less than one hundred years ago, when all women over the age of 21 won the right to vote in 1928.viii Over the last century, citizens of democratic states have won a voice in many areas of policy that affect us all such as education, sexual and mental health, environmental issues. We can see from this short history of monetary reform that problems with the money system were always debated amongst a small elite of (mostly) male bankers, economists and politicians and the 2008 financial crisis made it clear that monetary policy, which profoundly affects all other areas of public life, is maybe the last bastion of policy not truly under democratic control.

A ‘democratic deficit’ describes a situation where institutions claiming to be democratic do not act according to democratic principles of representation. This is most clearly the case in the area of monetary policy. In all the centuries of elite debate, the basis of a monetary system in which privately owned, profit-seeking banks create most of the money supply through interest-bearing loans has never been called into question. It is taken as a given and all economic policy is based on it. No alternatives are seriously considered.

For many years such issues and proposals for reform were debated on the fringes of society by small groups of concerned citizens such as: Christian Council for Monetary Justice; Forum for Stable Currencies; Prosperity UK with its annual Bromsgrove conference.

After the financial crash of 2008, a new campaigning group emerged called Positive Money, which has been very successful at reaching a much wider audience with monetary reform ideas by smart use of modern media. Positive Money highlights the economic problems created by reliance on the private banking system to create most of the money supply and proposes giving government the powers to create interest-free, debt-free money for the public benefit. There is now an International Movement for Monetary Reform.

In November 2014, the UK Parliament debated money for the first time in 170 years. ix

Seven MPs spoke at the debate, 12 MPs asked questions and another 15 were in attendance out of a total of 650 MPs. This historic debate has so far produced no concrete proposals for reform from the Parliament of a country suffering the ravages of deeply contested austerity policies, in a world holding its breath for the next big financial crash.

Whether reformers are campaigning for changes in the national monetary system, for banking reform or for alternative systems such as regional and virtual currencies, they will need to work harder to reach both hearts and minds with arguments and strategies that are believable and workable – economically, technically and politically.

It took thirty years from the first anti-slavery debate in the House of Commons until William Wilberforce and his colleagues saw victory with the first anti-slavery legislation. We can only hope it does not take so long to free us from financial slavery to big banks and their unjust grip on the financial system and we create a monetary system that is truly under democratic control for the first time in history.

In my next post I will take a more detailed look at the proposals of Positive Money and another campaign “QE4 People”. Will they prove GK Galbraith wrong, quoted at the start of this post? Or will the ‘remedy’ be a source of new abuse?

i Glyn Davies, A History of Money, University of Wales Press, (1994), p. 29-30

ii Stephen Zarlenga, The Lost Science of Money, American Monetary Institute (2002), p. 215-217

vi Glyn Davies, A History of Money, University of Wales Press, (1994), p.293

vii Glyn Davies, A History of Money, University of Wales Press, (1994), p.380